Insurance is no one’s favorite topic. We all have it, but understanding what your policies cover and why you need it can be confusing for even the most seasoned homeowner.

Have you been wondering:

- If your homeowner’s insurance policy is appropriate for your home?

- How to file a claim when needed?

- What are the big risk factors for your home?

Today, we’re breaking down all of the homeowners insurance claims statistics you should know and understand in order to make an informed choice for your property and family.

Importance of Homeowners Insurance

Your home is one of the most valuable things you own. As such, you want to protect it properly.

Homeowners insurance helps you prepare for the worst. Life will inevitably through hurdles your way. A good homeowners insurance policy can be the difference between smooth and speedy repairs and a headache and anxiety.

Homeowners insurance pays for damage to your property in the case of natural disasters, accidents like fires or plumbing issues, or robberies.

5 Types of Homeowners Insurance Coverage

Most home insurance policies will include coverage for your home and attached structures. Depending on your situation, you may choose to add on different types of coverage to protect your home from a variety of situations.

Interested in exploring the different types of coverage available to you? Here are some of the main types to look out for.

1) Dwelling Insurance 🏠

Dwelling coverage typically takes care of any damage your actual house incurs. This includes attached structures, like garages. Most homeowners insurance policies include this type of coverage.

2) Personal Property 💍

Personal property damage claims will help you in the event that your possessions get damaged or stolen. This could help cover water-damaged furniture, smoke-damaged clothes, or stolen electronics.

3) Flood Insurance 🌊

Flood insurance will protect your home from damage to your home’s structure or your personal belongings in case of a flood.

4) Earthquake Insurance 💥

Earthquake insurance is a must-have if you live in an area that is susceptible to earthquakes. This will cover damage to your home and some items as well.

5) Other Structures 🛖

This policy protects structures on your property that are not attached to your home. This includes structures like sheds and fences.

Homeowners Insurance Claims Statistics

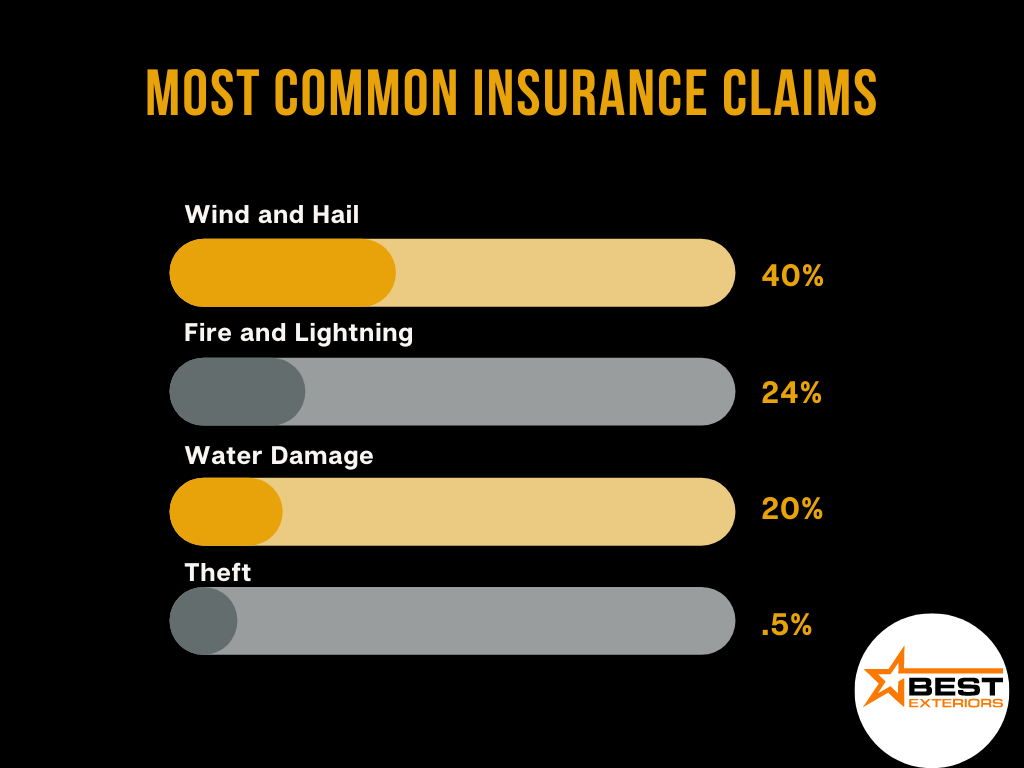

Common Causes of Property Damage

When it comes to homeowners insurance, some claims get filed more frequently than others.

- Wind And Hail Damage 🌪️ – Wind and hail damage are by far the most common home insurance claims. Common problems from wind and hail include blown-off shingles, dents in your siding, and damage to your roof or windows.

- Fire and Lightning ⚡️ – With droughts and rising temperatures, fire and lightning damage are becoming more common, beating out water damage. As natural disasters such as wildfires increase in frequency, homeowners may want to consider that when purchasing their insurance policies.

- Water Damage 💧 – Water damage can come from a variety of sources, including heavy rainfall, flooding, or frozen and burst plumbing.

- Theft 🦹🏻 – While theft-related claims have gone down over the years, they remain one of the top claims made by insurance policyholders.

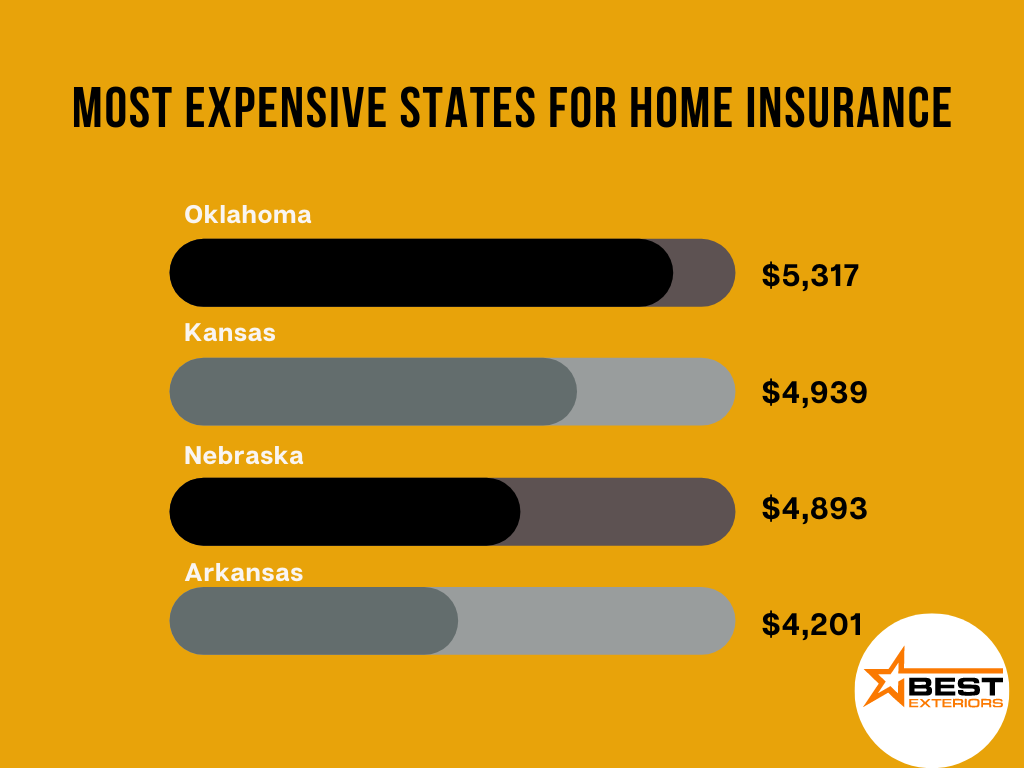

Homeowners Insurance Rates By State

When it comes to pricing insurance, there is a surprisingly wide gap between the most expensive state and the least expensive.

There are several reasons why a state may have unusually high insurance rates. For example, Oklahoma, which has had the highest insurance rates for many years running, has some specific risks for homeowners. Namely, it is located in the famously named “Tornado Alley,’ This high risk of tornado damage, as well as risk from frequent wildfires, significantly raises the average cost of insurance in the state.

While the risk from natural disasters tends to raise insurance rates, interestingly, states like California and Hawaii have significantly lower rates, despite having a similar or higher risk of damage from weather-related events than other states on this list.

This is likely because lawmakers in those states have created specific policies to help lower homeowners’ insurance rates. For example, in Hawaii, homeowners are required to purchase separate policies to protect them from hurricane damage. This lowers the overall price of homeowners insurance, statistically, but it may even out when it comes to the total amount paid for insurance policies.

When to File a Claim

Standard advice tells you to contact your insurance policy holder as soon as your house has been damaged.

However, there are circumstances where it is not in your best interest to file a claim right away. When the insurance company pays for the damage to your home, it will likely raise your annual premium, which might cost you more in the long run.

Instead, we recommend first taking pictures of all of the damaged areas of your home. Afterward, it may be worthwhile to do a little research to see how much it will cost to repair the damage on your home out of pocket. You may find that it is a more affordable option than you think.

Prepare Your Home With a Pro

One of the best ways to avoid having to make expensive insurance claims in the first place is to protect your home from property damage before it happens.

Our team at Best Exteriors are experts in protecting your home from environmental damage. From installing sturdy siding to helping you choose a roofing system that works for your environment, our team of professionals will help you create a home that stands up to all weather conditions.Want to learn more? Contact us today to set up your free consultation!